As a follow-up to my recent blog about the difference between your income or profit and loss (P&L) statement and balance sheet, I want to dive a little deeper into how to troubleshoot some common cash flow problems.

Your statement of cash flows (SCF), also called a cash flow statement, is part of the three-pronged approach to financial reporting. It reports your cash in terms of its operating, investing and financing activities. The SCF is an underused report and a perfect tool for troubleshooting cash flow issues. Think of it as the bridge between your balance sheet and P&L. Start with your SCF and work backwards from there to troubleshoot your cash flow problem.

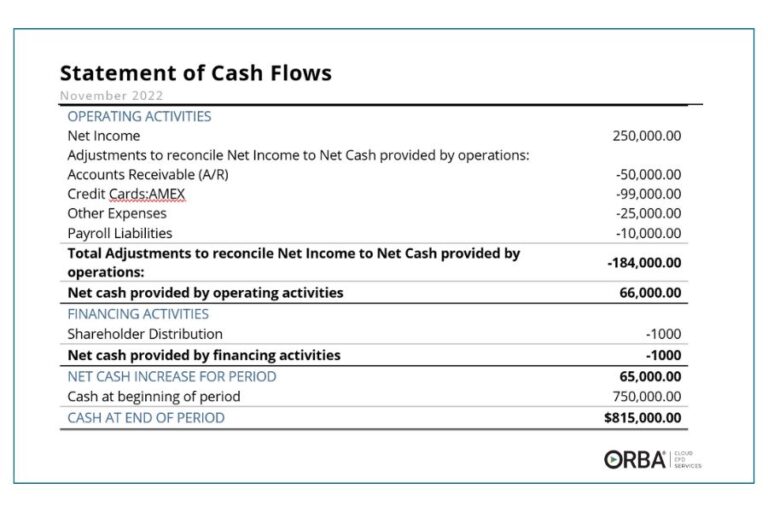

Related Read: What is a cash flow statement and why is it important?

For example, take the SCF of a consumer products company with a high volume of inventory. It is reporting a poor cash flow balance. Working backwards, the balance sheet illustrates an increase in current assets from the investment it made in inventory—every entry on the balance sheet is a placeholder for something that has not turned into cash yet. It should then be clear that the company’s closing cash balance is small due to the business’ investing and operating activities.

Common Cash Flow Problems

There are any number of explanations why a company may be experiencing cash flow issues. The most obvious reason is operating at a loss.

More interestingly, if your P&L is positive and you are still having cash flow problems, that is when the statement of cash flows becomes really useful. It could highlight:

- A growing AR balance;

- A growing inventory balance;

- Big investments needed in fixed assets; or

- High debt repayments.

You may be wondering where to look to determine if any of the issues above are affecting your cash flow, and if so, what you should do. These are the top five cash flow problems we see among new and prospective clients and a few suggestions for ways to fix them:

Operating at a Loss

Key Metric: Net Profit Margin

Where to Look: P&L

If your income is really a loss (i.e., if your P&L is negative), your business is not profitable.

Troubleshooting Tip: Focus on your P&L. Look to see where you might be spending too much or if sales are down, dig into those drivers and the reason why. It is also good to know it is possible to have a positive cash flow, even if your business is operating at a loss.

Growing Accounts Receivable (AR) Balance

Key Metrics: Balances Past Due, Customers Owing, DSO

Where to Look: Balance Sheet

Troubleshooting Tip: To troubleshoot this cash flow problem, run AR aging reports. For example, balances past due, customers owing or DSO (days sales outstanding) metrics. Slow AR cycles may be hidden from your P&L, but should become apparent on your balance sheet. There are many ways you can improve your AR cycle, but a few quick fixes involve establishing firm payment terms and/or making it easy for customers to pay you by offering multiple and instant payment channels.

Growing Inventory

Key Metric: Inventory Turnover

Where to Look: COGS can be found on your P&L

Troubleshooting Tip: Look at the trend of your inventory turnover metric (KPI), or COGS divided by your total inventory. This will let you know if you are buying more inventory than you are selling, or if you are buying inventory too fast. Then, break that metric down further: Take inventory and separate into different product groups and look at turnover individually to determine which groups are stale. Next, determine how to sell the excess inventory for cash, even if it is at a discount. Try to stock more inventory that sells quickly to troubleshoot this cash flow problem. A faster inventory turnover equals increased cash flow.

Too Many Fixed Assets

Key Metric: Net Fixed Assets

Where to Look: Balance Sheet

Troubleshooting Tip: Cash used toward investing on fixed assets can leave you cash poor. One way to troubleshoot cash flow issues due to fixed assets is searching for alternatives to buying equipment like renting or leasing.

A recurring expense can also sometimes be hidden as a fixed asset. You will catch it by looking at your balance sheet. Generally, when buying equipment, these are not recurring items; it is a large amount of cash, upfront, one time. If you are continually spending cash on these items, it may not actually be a fixed asset and should instead be moved to your P&L as an operating expense.

Debt Repayment

Key Metric: Debt-to-Equity Ratio

Where to Look: Balance Sheet

Troubleshooting Tip: Paying off debt is a great example of when a company might actually be financially healthy but have a low cash flow. Usually, only the interest on your debt is showing up on the P&L, but when you are paying off the principal as well it will affect your cash flow. If your company continues to pay off debt over time, your debt-to-equity ratio will be decreasing, which is a good thing. Keep in mind that it is important to also consider the drain on cash flow from higher interest rates on short-term debt compared to interest on long-term debt.

Not all cash flow issues are problems

It is possible to have limited cash flow but still be in a financially stable position. Using the consumer products company from earlier as an example: The company’s SCF reports a small cash flow balance but the organization is growing assets in inventory. If the company made $3 million YTD compared to $800,000 last year and is simultaneously using the revenue gain to pay off debt while investing in inventory, it has a small amount of cash but is, in reality, improving its financial health.

Addressing your cash flow issues for the big picture.

Troubleshooting common cash flow problems should almost always start with the statement of cash flows and then be focused on working backwards through your balance sheet and P&L to determine the root cause of your issues. Once you have revealed the reason for your cash flow problems, you can dig in deeper using the most relevant KPIs. By bridging your three financial statements, you can determine the drivers and ratios needed to make assumptions and forecasts for growth.

Need help building out your three-pronged approach to financial reports? Our controller services are designed to do just that.