New clients frequently ask us how to best organize their neglected books. And, it’s often the first place we start when we’re onboarding new clients. The truth is, the sooner you clean up your books, the sooner your outsourced accounting team can focus on growth. Growth is awesome, bad bookkeeping habits are not.

Break these six bad bookkeeping habits before you find yourself drowning in disorganization.

The top 6 ways to clean up your books:

1). Ignoring inefficiencies.

We’re going to do away with suspense and start with the worst culprit for dismantling good bookkeeping: Inefficiencies. As a virtual accounting team, we are determined to find ways to optimize our time and productivity. It is an ongoing mission. Always. And to be frank, the accounting profession is not always the best at this. Which is why we make it even more of our mission. So, where to start?

Step 1, move your accounting to the cloud.

This allows for easy anytime, anywhere access. It also avoids those old-school remote desktop connections that require hosting on your server and a complex, time consuming login process. As a bonus, many cloud software solutions also have a phone app that lets you see real-time dashboards wherever you are (because we know you don’t have time to just sit in front of your computer all day.)

Step 2, find systems that play nicely together as they have seamless integrations.

This will save you time – see #3 for more about this. If a seamless integration is not available, at least utilize an export/import process for keeping systems in sync so you do not have to manually enter a bunch of data. Data entry is not awesome.

Step 3, use Excel’s Pivot Table capabilities.

Why do so many old school accountants still NOT know how to use this, despite it being around for more than two decades? Pivot tables let you summarize and slice and dice a large volume of data very quickly to help you turn your data into information. After all, that is the real purpose of accounting, right?

2). Avoiding risk management and internal controls.

This is a serious subject in the accounting field. Yes, risk management and internal controls are important. Yes, you need the proper procedures in place. But, do not ignore #1 above to accomplish them. With the right team of professionals and the right tools in place, you can have both efficient systems and strong internal controls. Plus, if the cloud solutions above are set up correctly they can actually help increase your internal controls; like mitigating your risk of expense report fraud for example. If you don’t have solid internal controls, then all you can do is hope that your financials are accurate and that nobody is skimming anything from you.

3). Not syncing your integrations.

Ok, now we are just beating the same old drum. But, it’s worth repeating. Traditionally, accounting and tech have not meshed well. However, that is quickly changing in this great new era of cloud services. Talk to your accounting professional if you are not sure how your ERP, inventory system, payment gateway, or SaaS billing system speak to your accounting software. If you can’t find a way to sync your existing systems, our outsourced accounting for SaaS companies or ecommerce accounting services can suggest ways to streamline your financial operations and get you the financial reports that will help your business scale.

4). Steering clear of procedures and standardized reporting.

Meh, meh, meh. Even the subheading is boring. Procedures are rarely anyone’s idea of a good time. That being said, even the most modern accounting team has a place for procedures. With the appropriate processes in place, you can clean up your books in a surprisingly automated way. Having standardized reporting is one of the top 5 benefits of outsourcing bookkeeping services.

Quick Cloud CFO tip: Standardizing your monthly financial reporting and processes may seem like an obvious step, but surprisingly it is one that is missed frequently by startups and young businesses. Start by creating some processes around the following reports:

Your Accounts Receivable and Aging Reports

Pay attention to your aging reports and your accounts receivable.

If you aren’t collecting your cash, then you’re not a real business. That is a very simplified statement. But, if your accounts receivable is running way behind this directly affects your cash flow. And these days, more than ever, cash is king.

Related Read: 6 ways you can start improving your accounts receivable today.

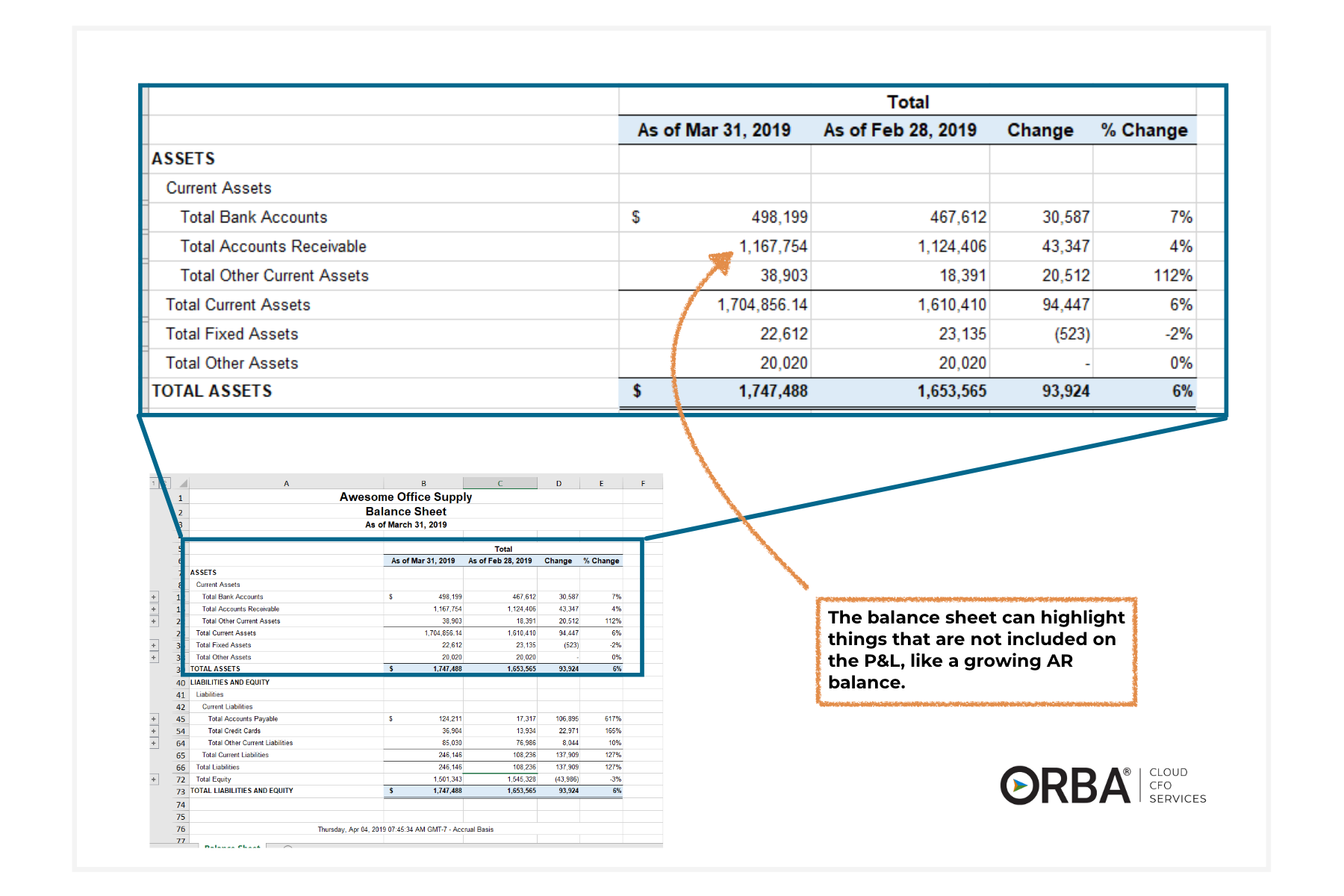

Your Balance Sheet

Don’t ignore your balance sheet.

This is a big one. We often see companies only drilling down on their profit and loss statement (P&L) without realizing they could be missing a lot of important items that never hit their P&L. Your balance sheet demonstrates how effectively your company is turning its profits into cash. For example, you might not realize you’re missing some big items that affect your cash flow if you’re spending a lot of cash on inventory or fixed assets.

The metrics found on your balance sheet help identify trends so you can adjust operations as needed to “balance” your risk and return.

Finally, document financial processes.

This might be one the #1 ways to clean up bookkeeping. And it’s another one of the early steps we take when we’re onboarding new clients because a huge majority of small businesses come to us without proper bookkeeping documentation.

We like to use Asana to document all of our daily, weekly, monthly, quarterly, and annual tasks. This way, the built-in reminders of Asana let us know what needs to be done and by when. It also serves as a knowledge base of all procedures so we can address employee turnover more easily. Plus, as part of our standard outsourced bookkeeping services, it’s a huge value-add for you because you finally have all your financial processes documented.

5). Procrastinating.

No one likes a procrastinator. Especially your books. Do not forgo your account reconciliations for a rainy day because—let’s be honest—that rainy day is not coming. If you are a successful entrepreneur, you do not (and will not) ever have time to go back and complete retroactive reconciliations. Your reconciliations can easily be outsourced to an outsourced bookkeeping service so that you can focus on growing your business. If your accounts are not reconciled, then you can never truly know that your reporting is accurate or reliable. It’s like racing a car while only looking in your rear-view mirror.

6). Not realizing it’s time to hire a pro.

There comes a time in most business’ growth when a company will require professional advice. We have found tax savings for clients who were not aware they were eligible for the R&D tax credit. Other clients were incorrectly assuming they had more cash flow than they did and were happy to have us step in and help them see their whole financial picture before they ended up cash-poor. Remember, the money you save in hiring a professional can pay for their cost. But, more importantly, a professional can help you scale your business faster and more profitably. Finally, the pros can handle those “super-fun” tasks like reconciliations so that you stop falling behind, which allows you to focus on other aspects of your growing business.

Let’s be honest, nobody really wants to clean up their bookkeeping but, hopefully, we’ve made it clear why you should.

Related Read: How do you know if you need to hire a controller or a CFO?

Feeling overwhelmed with messy books? Don’t know where to start? Contact us to find out what clean-up and onboarding looks like for a business like yours.